By Gregor Smith, Queen’s University

The Canadian dollar (CAD) often is described as a ‘commodity currency’ or even as a ‘petrocurrency’. The correlation between commodity prices and the value of the CAD features in daily commentary but you can see it in data at any frequency.

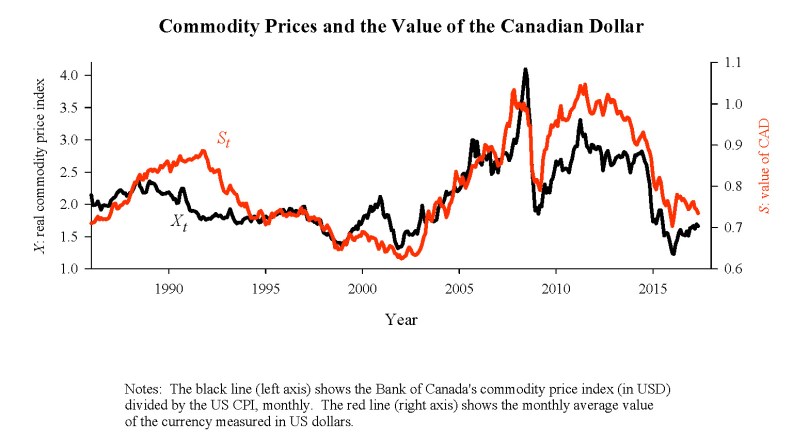

The figure below shows monthly data for the CAD/USD exchange rate along with the Bank of Canada’s commodity price index (reported in real USD) over the past thirty years. Clearly, these two things tend to move together.

The same correlation is evident if we isolate the energy component of the price index. And the correlation also appears for other countries like Australia and New Zealand. Their largest exports are iron ore and dairy products respectively although, for some reason, calling the AUD a ‘ferrocurrency’ or the NZD a ‘lactocurrency’ hasn’t caught on. For these small(ish) open economies we think of these commodity prices as being determined in the world at large, so it seems natural to think of causation running from them to the exchange rate.

Is the source of these correlations obvious? It is not obvious to me and my colleague Michael Devereux from UBC. We find it difficult to tell a traditional supply-demand story that yields this correlation. Moreover, the foreign exchange market simply seems too large to be influenced by events in markets for goods and services or even equities. The BIS triennial survey (April 2016) reports the daily average turnover for the CAD against the USD: It is 218 billion USD. These daily volumes of foreign exchange transactions dwarf daily trade flows, daily GDP, or daily transactions values in stock markets. For example, the average daily value of transactions on the TSX in 2016 was 4.7 billion USD. And quoting Canada’s 2016 annual exports by dividing by the number of trading days on the TSX (258) gives a mere 1.84 billion USD per day.

Our hypothesis instead has two parts. First, the exchange rate reacts to differential monetary policy across countries and also to expected future values of this differential. So if foreign exchange markets believe the Bank of Canada will raise its overnight interest rate relative to the US federal funds rate then the CAD will appreciate now. This is simply the idea that the foreign exchange market ‘discounts’ future fundamentals (here in the form of an indicator of relative monetary policy) when they are forecasted in advance.

Second, Canada is a commodity exporter, so an increase in commodity prices is an early warning of future inflation and growth. Thus the inflation targeters at the Bank of Canada react to it in setting monetary policy. Knowing this pattern, traders bid up the value of the Canadian dollar when commodity prices rise.

We find this pattern in the past thirty years of data for Canada, Australia, and New Zealand. An increase in the commodity price index is followed by an increase in the central bank’s policy interest rate. More strikingly, once we control for the feed-through from these anticipated increases in interest rates on the exchange rate, there is no statistically significant, remaining effect of the commodity price on the exchange rate. It appears to all be mediated through relative monetary policy.

Who cares? A perennial question for countries with floating exchange rates is whether the big swings we see in currency values make some sense after the fact, even if they cannot be forecasted in advance. We certainly don’t claim to explain all the movements in these three exchange rates. But we do think there is a simple explanation for the commodity currency correlations and one which fits with a longstanding view of the effects of monetary policy.

References

Bank for International Settlements (2016) Triennial Central Bank Survey: Foreign exchange turnover in April 2016. https://www.bis.org/publ/rpfx16fx.pdf

Devereux, Michael B. and Gregor W. Smith (2017) Commodity currencies and monetary policy: A simple test. Mimeo, Department of Economics, Queen’s University

http://qed.econ.queensu.ca/pub/faculty/smithgw/DevereuxSmithOctober2017.pdf