By James McNeil, Queen’s University

The nominal interest rate can be decomposed into the sum of the real interest rate and expected inflation through an economic relationship called the Fisher equation. While monetary policy typically works by adjusting short-run nominal interest rates, economic theory suggests that it is the real interest rate that influences borrowing and lending decisions. How much of an adjustment to the nominal interest rate passes through to affect the real interest rate – and hence the real economy – will depend on the response of inflation expectations.

Furthermore, central banks may wish to directly influence inflation expectations to avoid falling into a liquidity trap or to achieve additional stimulus when nominal interest rates are exceptionally low. In 2009 the Federal Reserve lowered its policy interest rate to zero, which is considered to be the lower limit, effectively losing its main policy tool. In response, it turned to unconventional monetary policy operations such as forward guidance (promising to keep interest rates low for an extended period of time) and large-scale asset purchase programs (often referred to as Quantitative Easing). If these unconventional policies are able to directly move inflation expectations when short-run nominal interest rates are constrained then the Federal Reserve would have the means to affect real interest rates when its preferred policy tool is not available.

In my research, I estimate how inflation expectations in the United States (taken from the Survey of Professional Forecasters) respond to monetary policy actions, both conventional and unconventional, from 1992 to 2018 [1]. I use the unobserved components model [2], which decomposes inflation expectations into a permanent component representing long-run inflation expectations and a temporary component representing short-run expectations. Expectations of inflation at any horizon, as well as the change to these expectations after a monetary policy shock, can then be constructed from just these two components and model parameters.

One challenge to estimating this model directly from the survey data is that the professional forecasters may not produce forecasts that are consistent with underlying inflation expectations. Recent work by Coibion and Gorodnichenko (2012,2015) provides empirical support for models with information frictions, which can explain why forecasters appear to make errors in a systematic manner. To account for this I modify the unobserved components model to accommodate two information frictions: a sticky information channel [5], which can explain why forecasters are slow to respond to new information, and an anchoring channel [6], which can explain why forecasters place too much weight on long-run expectations. Each friction is statistically significant over the sample period.

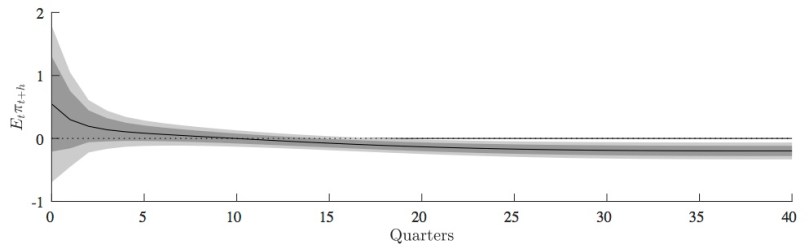

Figure 1 shows the dynamic response of inflation expectations after a monetary policy tightening normalized to increase the one-year treasury bill rate by 100 basis points. We see that the higher interest rate decreases inflation expectations after a lag of several years. Additionally, my analysis shows that the negative response shown in the figure is driven by the long-run component of inflation expectations, which declines by approximately 20 basis points upon impact and the effect is permanent. In other words, temporary monetary policy actions have a permanent effect on the level of long-run inflation expectations. This is clear from the figure where we see that the effect is significant even 10 years after the policy action.

Figure 1: Response of inflation expectations to a monetary policy shock

One implication of this finding is that long-run inflation expectations are more variable than is often assumed. We may think that, if the Federal Reserve has a credible and well-understood inflation target, then long-run expected inflation should be stable at this level. Instead, we see that long-run expectations respond to monetary policy changes.

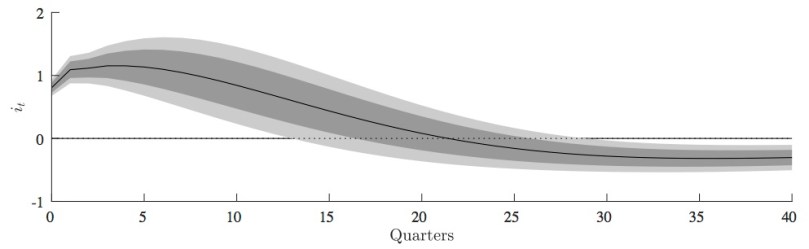

A second implication has to do with the effect on future interest rates. Figure 2 shows the dynamic response of the interest rate on one-year treasury bills after the same monetary policy action. We see that the interest rate first increases after the monetary policy change and remains significantly higher for several years. Eventually, however, the interest rate declines, and it remains significantly lower even ten years after the policy change. Recalling that nominal interest rates are linked to long-run inflation expectations through the Fisher equation, the long-run effect on interest rates is being caused by the response of long-run inflation expectations. This is the effect of the inflation expectations channel; higher interest rates today cause lower interest rates in the future by lowering long-run inflation expectations.

Figure 2: Response of interest rate to a monetary policy shock

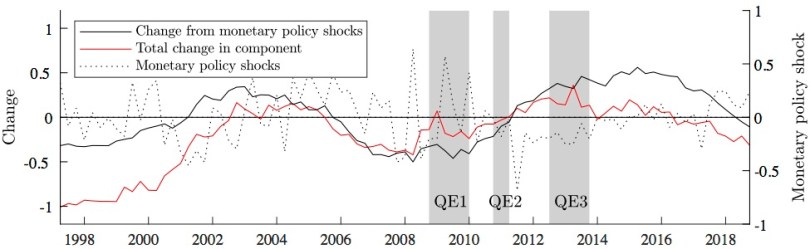

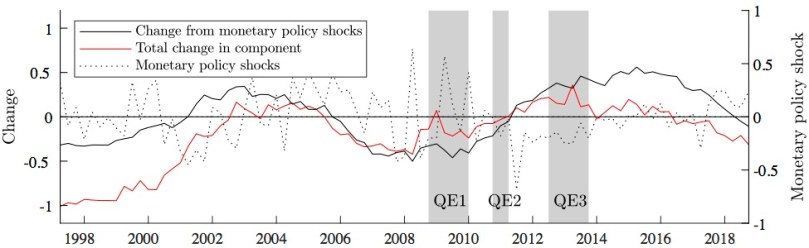

I also show that monetary policy explains a significant fraction of the variability in long-run inflation expectations. The solid black line in Figure 3 shows the cumulative effect of the current and previous 20 monetary policy shocks on long-run inflation expectations. For comparison, the red line shows the total cumulative change in long-run inflation expectations over the same period and the dotted line shows the underlying monetary policy shocks (right axis). The grey shaded areas correspond with the timing of the Federal Reserve’s asset purchase programs.

Figure 3: Historical decomposition of long-run inflation expectations

In 1997 the total cumulative change in long-run inflation expectations over the previous five years was a decline of 100 basis points, about one-third of which can be explained by monetary policy actions undertaken during that time. Beginning in 2004 we see the red and black lines begin to move together more closely which indicates that monetary policy is explaining more of the dynamics of long-run expectations.

Of particular interest is the sustained upward pressure monetary policy placed on expectations between 2009 and 2014. Because conventional monetary policy was constrained during this time, we can attribute this effect to unconventional policy actions (forward guidance and asset purchase programs) which helped to prop up long-run inflation expectations through this period. Because nominal interest rates were constrained during this time the increase in long-run inflation expectations would have put downward pressure on real interest rates, providing additional stimulus to the economy through the recession and recovery period.

This indicates that unconventional monetary policy actions are able to move long-run inflation expectations which can provide additional monetary stimulus by lowering real interest rates in the event that nominal interest rates are constrained at their lower bound.

References

[1] McNeil, J. (2019). Monetary policy and the term structure of inflation expectations with information frictions. Mimeo, Department of Economics, Queen’s University.

[2] Stock, J. H. and Watson, M. W. (2007). Why has US inflation become harder to forecast? Journal of Money, Credit and Banking, 39(s1), 3–33.

[3] Coibion, O. and Gorodnichenko, Y. (2012). What can survey forecasts tell us about information rigidities? Journal of Political Economy, 120(1):116–159.

[4] Coibion, O. and Gorodnichenko, Y. (2015). Information rigidity and the expectations formation process: A simple framework and new facts. American Economic Review, 105(8):2644–2678.

[5] Mankiw, N. G. and Reis, R. (2002). Sticky information versus sticky prices: A proposal to replace the New Keynesian Phillips curve. Quarterly Journal of Economics, 117(4): 1295–1328.

[6] Patton, A. J. and Timmermann, A. (2010). Why do forecasters disagree? Lessons from the term structure of cross-sectional dispersion. Journal of Monetary Economics, 57(7):803–820.