By James McNeil, Queen’s University

The nominal interest rate can be decomposed into the sum of the real interest rate and expected inflation through an economic relationship called the Fisher equation. While monetary policy typically works by adjusting short-run nominal interest rates, economic theory suggests that it is the real interest rate that influences borrowing and lending decisions. How much of an adjustment to the nominal interest rate passes through to affect the real interest rate – and hence the real economy – will depend on the response of inflation expectations.

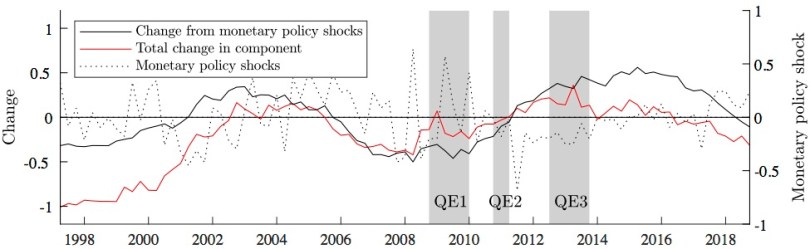

Furthermore, central banks may wish to directly influence inflation expectations to avoid falling into a liquidity trap or to achieve additional stimulus when nominal interest rates are exceptionally low. In 2009 the Federal Reserve lowered its policy interest rate to zero, which is considered to be the lower limit, effectively losing its main policy tool. In response, it turned to unconventional monetary policy operations such as forward guidance (promising to keep interest rates low for an extended period of time) and large-scale asset purchase programs (often referred to as Quantitative Easing). If these unconventional policies are able to directly move inflation expectations when short-run nominal interest rates are constrained then the Federal Reserve would have the means to affect real interest rates when its preferred policy tool is not available.Read More »